Partner Article

Are Retirement Savers about to face a Crisis?

A looming State Pension funding crisis could have severe consequences for those saving for retirement, if action is not taken. Paul Gilsenan, Principal of Paul Gilsenan Wealth Management – a Partner Practice of St. James’s Place Wealth Management – explores the need for retirement savers to make the most of available reliefs and allowances.

Philip Hammond may have claimed in his Spring Statement that “there is light at the end of the tunnel” in rebuilding the UK’s finances, yet a paper published by the Government Actuary’s Department (GAD) has uncovered a potential hole in the public purse that could mean that the National Insurance Fund – from which State Pension payments are made – will run out in the early 2030s.

The report identifies a mismatch between the amount of money coming in through National Insurance contributions (NICs) and the amount going out in benefits – over 90% of which is absorbed by the State Pension.

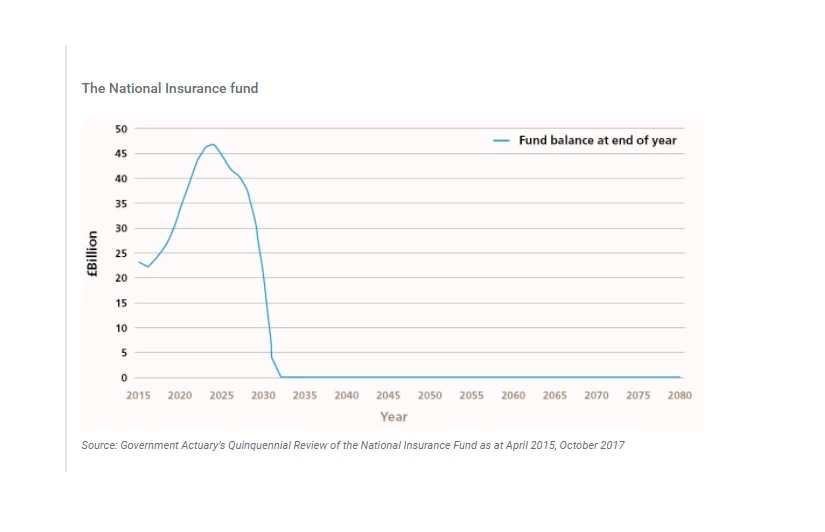

What does the future hold?

The balance of the fund currently stands at around £25 billion. Indeed, the short-term picture looks fairly healthy, as factors such as the rising State Pension age boost NIC receipts. However, the declining ratio of those in work to those in retirement, and the impact of the State Pension triple-lock – which guarantees that payments rise in line with the highest of average earnings, inflation or 2.5% – sees the size of the fund plummet from 2025 onwards. Under current assumptions, the fund will be exhausted from around 2032.

“If the system is to continue to cover the current form of State Pension and other benefits, then either the fund’s income has to rise or expenditure has to be controlled,” says Martin Lunnon of GAD.

State Pension funding – a looming crisis?

To continue paying the State Pension in its current form, the government must find an extra £11.6 billion by 2030, rising to £55.9 billion by 2040. How it responds to ensure that additional funds are found in time is now the key question.

In the wake of one of the longest and deepest financial squeezes in history, it’s hard to envisage cuts to key public services. Likewise, any further attempt to hike NICs is likely to spark the same firestorm that engulfed the Conservative Party a year ago, when it proposed changes for the self-employed. Indeed, “substantial increases in National Insurance contribution rates would both be particularly politically sensitive and would again require primary legislation,” notes GAD.

Against that backdrop, the government could be forced to look elsewhere. It is already proceeding with an accelerated increase in the State Pension age, and it’s quite possible that this will have to rise further and/or faster than the current timetable.

What are the consequences for savers?

The government could be compelled to cut back on allowances and benefits provided to savers. Tax relief on pension contributions has been at the mercy of cash-strapped chancellors for some time, but whether this government has the appetite to abolish the higher and additional rates remains to be seen. Nevertheless, it spent more than £50 billion on tax relief last year (HMRC statistics, 2018), prompting speculation that the system will be overhauled in the near future.

It may well see more ‘salami slicing’ as the answer. The annual allowance for pension contributions came down from £255,000 a year, to £50,000 then £40,000. However, some top earners can see their annual allowance reduced to just £10,000 under new rules. It’s quite possible that those earning more modest sums could see a reduction applied to their allowance in future, making it much harder for them to build a sufficient retirement fund.

Whatever happens, pension tax breaks for high earners are unlikely to become more attractive. It also seems inevitable that individuals will become increasingly responsible for funding their retirement as state benefits come under greater pressure.

What action can savers take?

As we approach the end of the tax year, those who can should try to take advantage of the generous reliefs and allowances while they are still available. This means making the most of this year’s annual allowance and carrying forward any unused allowances from the three previous tax years. That way, individuals can benefit from current rates of tax relief and potentially enjoy a higher income when they stop work.

This was posted in Bdaily's Members' News section by PSG Wealth Management Ltd .

Our Partners

The value of creating a stronger careers route

The value of creating a stronger careers route

Apprenticeships: Invest in talent or keep chasing it

Apprenticeships: Invest in talent or keep chasing it

Are you ready for salary transparency?

Are you ready for salary transparency?

Confidence the key to our artificial intelligence future

Confidence the key to our artificial intelligence future

The missing piece of the puzzle in the NEET crisis

The missing piece of the puzzle in the NEET crisis

The North East investment story needs two engines

The North East investment story needs two engines

We must forge change to close the skills gap

We must forge change to close the skills gap

Creating the conditions for North East talent to thrive

Creating the conditions for North East talent to thrive

Why local government is key to devolution success

Why local government is key to devolution success

Your reputation is worth more than that invoice

Your reputation is worth more than that invoice

There is no perfect time when selling a business

There is no perfect time when selling a business